Gainera2582

Power and Agility

- Location

- Lake Saint Clair, Michigan

The meaning of boat:

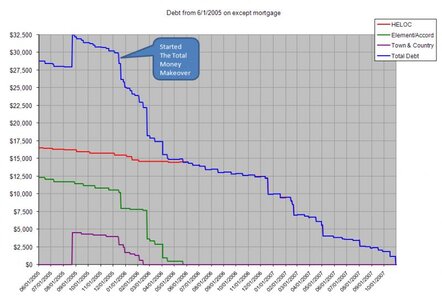

Bring out another thousand!!!!!

Bring out another thousand!!!!!

I would agree with the above. If it's unsecured debt (credit cards), you pay the card off with the highest rate first.

Doug

Question:

Would you pay more on a student loan that is at 2% interest or would you pay more on your mortgage thats at 6.~%? Mortgage is technically a 30yr but right now with my automatic payments it will be done in less than 12. Should I cut that payment back to the 15yr payment and put more towards the student loan? (I won't go less than the 15yr on the mortgage)

I also have money going into savings and also retirement that I could drop but these two are my only two loans and i won't be taking any other debt on so i prefer to build up some savings for emergency (currently about 3 months) and also put money into retirement while i'm young. Retirement is 10% now in 401K but plan to start the roth in a few months once I have the minimum balance saved up, then i'll be 15% between the two. 5% in 401k (match limit) and then 10% in roth.

Currently my student loan payment withdraws automatically and i dont really notice it so it doesn't bother me. If I would pay it off more aggressively, it would take 1.5 to 2 yrs and would substantially reduce some of my other efforts so I haven't wanted to. What do you think?

Dave Ramsey does not agree, and I don't either.

What is the balance on the student loan? By Ramsey's advice, if the student loan is over 1/2 your yearly income, then it would be paid off at the same time you pay your mortgage. If it's less, then you attack it now and save the mortgage for later.

boat? never ever ever ever ever ever. Holy Money pits. Every thing that breaks costs a fortune because it is a "marine part". F that.

Ask ski4 how much he uses his and how much it costs him a year. He could by a brand new decked out freestyle ski every single year.

Tell me why you would not pay off the highest rate card first?

Doug

Tell me why you would not pay off the highest rate card first?

Also, there is no problem with surfing a balance to a lower interest rate, as long as you close the old account and don't run up more debt.

I remember a call to Dave recently where a lady wanted to know if it was ok to surf a balance, and Dave said ok, but then he heard the balance and did the math, it was going ot save like $12 because they were almost done with it. $12 barely buys a pizza. Why bother.

I still don't agree with you Darin, but I'll agree to disagree.

Aren't most student loans terms a max of 10 years?

Doug

The Dave Ramsey method is mostly about FOCUS to pay it off, rather than math.

Spend all energy & focus to knock debt out. The easiest way to do that is to pay the smallest first.

First of all, I think there is some confusion going on here. You said smallest debt, not smallest/lowest rate. Am I misinterpreting your sentence?

This why I don't agree with Dave Ramsey. Yes, he does have some good things to say, but I personally deal with facts/logic, etc in regards to paying off debt. Paying off debts with lower interest rates vs. higher interest rates does not make logical sense.

If your highest rate card is whacking you with $120/month in interest and your smallest rate card is whacking you with $10/month, why would pay off the smallest rate card first? You could pay the minimum every month on the lowest rate card and the annual interest on that card would equal just one month's of interest on the highest rate card. Why again would you pay the lowest rate card? Just because Dave thinks it's going to make someone 'feel good' because they pay off a debt without logic doesn't hold up in my book.

Doug

You'd have to talk to someone to understand.

Like me, I cannot for the life of me figure out why people go to cash advance places, then just the 'loan' over, extend it, whatever, and keep paying like 10%/month or whatever it is. I've never been in that situation and/or I know enough about money to not do it. That person apparently doesn't, or just feels trapped, or whatever.

Some people consolidate student loans which extends them, etc.

The Dave Ramsey method is mostly about FOCUS to pay it off, rather than math.

Spend all energy & focus to knock debt out. The easiest way to do that is to pay the smallest first.

Besides....you're not talking THAT much money in interest saved with most balances.

Because for people that have multiple credit card balances to pay off, they need to form good money habits, and paying off from smallest first gives them a small sense of success that will reinforce that they're doing the right thing and they are more likely to succeed.

Many times the lowest interest rate is also the biggest balance, which to people that don't have good money habits is going to seem insurmountable, and they will probably give up before ever getting it paid off.

To someone like you that might have good money habits, it's hard to understand, but you have to put yourself in other people's shoes. I have led 2 FPU (Financial Peace University) classes and met a lot of people doing that, and saw this exact scenario play out with 2 different people.

One girl was a single teacher with no kids, had always just spent money to hang out with friends, etc etc. She had a student loan sitting there, had had it for years, and really didn't think she'd ever pay it off, but after getting rid of all her credit card debt she was already knocking it down and loved it.